August 18, 2019 – ABC This Week

TRANSCRIPT

ABC, MARTHA RADDATZ: I’m joined by Peter Navarro, the director of the White House Office of Trade and Manufacturing Policy. We appreciate you coming in this morning, sir.

PETER NAVARRO, DIRECTOR WHITE HOUSE OFFICE OF TRADE AND MANUFACTURING POLICY: Good morning to you.

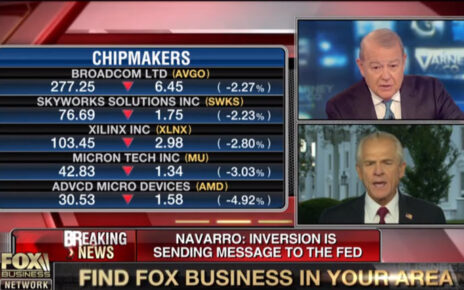

RADDATZ: We know the labor market is strong. We know consumer confidence remains high. But on Wednesday, we saw the worst drop in the stock market this year, and although there was some recovery there are indicators that the U.S. could be headed for a recession.

NAVARRO: So, before I came to the White House I spent a better part of 20 years forecasting the business cycle and stock market trends, and what I can tell you with certainty is that we’re going to have a strong economy through 2020 and beyond with a bull market, and here’s why, things are shaping well.

First of all, the Federal Reserve going into the holidays will be lowering rates significantly. What that will do it will help our investment directly and help our export indirectly through a currency effect. Secondly, the European Central Bank has signaled strongly they’re about to engage in a very aggressive round of monetary easing that will help not only revive the economy of Europe, but also help build export demand.

I think China is going to have a second round of fiscal stimulus. What that will do for the global economy is help the developing countries that sell them all the commodities for their manufacturing machine.

By early October, if congress rises above partisan politics, we should have passage of the U.S.-Mexico-Canada trade agreement. This is without hyperbole, the largest trade deal ever in history. It’s also going to give us hundreds of thousands of more jobs, more growth points, and there is a couple of other things I should mention…

RADDATZ: But these seem like a lot of ifs. If this happens, if that happens.

NAVARRO: The Fed will be lowering rates. The ECB will be engaging in monetary stimulus. China will be engaging in fiscal stimulus. You’re absolutely right, there’s also an if associated with the USMCA.

There also is an if with Brexit over in Europe. This is important, because that has suppressed investment in Europe. I think, by October 30th that situation is going to be resolved one way or the other.

RADDATZ: Let me talk about…

NAVARRO: So things are shaping up well for stimulus worldwide.

RADDATZ: Let me talk about these indicators, though, the so-called inverted yield curve. The yield curve has inverted before every U.S. recession since 1955. There was one false flag. Even though it may be brief…

NAVARRO: Yes.

RADDATZ: … how can you be so confident?

NAVARRO: I love to talk about the yield curve.

I didn’t write the book on the yield curve, but I actually wrote several books on the efficacy of the yield curve as a leading economic indicator.

RADDATZ: But let’s talk about that an indicator.

NAVARRO: Now, first of all, we did not have a yield curve inversion right now, by technical standpoints. You have to have a significant spread between short and long rates.

All we have, Martha, is a flat curve.

RADDATZ: I know you have talked about the flat.

NAVARRO: Flat.

RADDATZ: And, again, if this was only a brief inversion or it was flat, you’re still not worried about that?

NAVARRO: It’s a very weak signal. But it is flat, not for — for bad reasons, but for good reasons.

We have the strongest economy in the world. Money is coming here for our stock market. It’s also coming here to chase yield in our bond market. Now, what that does is, when foreign money comes in, it drives the prices of bonds up and yields down. That flattens the curves.

So, all what needs to happen here, Martha, is for the Federal Reserve to do what it needs to do, which is begin lowering interest rates. There’s a general consensus now on Wall Street and everywhere else in this country that the Fed raised rates too far, too fast.

We came in at Q2 at 2.1 percent GDP growth rate. We should have been at 3. And the Federal Reserve’s precipitous interest rate hikes actually cost us a full point of growth.

All we need, Martha, is to reverse that, have Europe do what they need to do, China do their fiscal stimulus, and the global economy will — will have a bullish cycle going through 2020 and beyond.

RADDATZ: But let me — let…

NAVARRO: That’s my message to the American people.

RADDATZ: Let me tell you what they — as I’m sure you’re well aware, “The Wall Street Journal” editorial board this month dubbed this the Navarro recession.

And they wrote a second editorial this week called “The Navarro Recession II,” saying: “Mr. Navarro and President Trump spent Wednesday blaming the Federal Reserve for the market meltdown, and we suppose any scapegoat will do in a storm. We have been warning for two years the trade wars have economic consequences, but the wizards of protectionism told Mr. Trump not to worry. The key to avoiding the worst is to restore a sense of policy, calm and confidence.”

And I would add to that, businesses are not blaming the Federal Reserve. For example, the National Retail Federation explicitly said uncertainty for business and the new tariffs will result in higher costs for consumers and slow the U.S. economy.

So, clearly not everyone agrees with you.

NAVARRO: So, let’s start with “The Wall Street Journal.”

When the Main Street journal starts attacking this administration, that is when we worry.

The question for “The Wall Street Journal” is, where was “The Wall Street Journal” beginning in 2001, when China got into the World Trade organization, and we watched the exodus of over 70,000 of our factories, over five million manufacturing jobs?

Why hasn’t “The Wall Street Journal” been editorializing over the last 10 years about China’s hacking our computers to steal trade secrets, about stealing our intellectual property, about forcing the technology transfer from our companies, about the currency manipulation that occurred for over a decade?

So, “The Wall Street Journal,” look…

RADDATZ: We don’t have a trade deal, though. And…

NAVARRO: It’s called — it’s called “The Wall Street Journal” for a reason. OK? It represents Wall Street.

RADDATZ: I — I…

NAVARRO: And “The Wall Street Journal” never saw an American job it didn’t want to offshore.

RADDATZ: Well, let’s talk about tariffs, which has consumers concerned and has businesses concerned.

NAVARRO: Sure.

RADDATZ: The president delayed some of those tariffs until after Christmas.

Why would delaying tariffs help American consumers, when the president and you have said that China is bearing the brunt of the tariffs?

NAVARRO: I love this question.

We have $300 billion worth of Chinese exports that did not yet have tariffs. So what the — what the president did was looked at that, and, as of September 1, about half of that will be tariffed at 10 percent.

Now, the other half, why didn’t we tariff the other half? One of the things the president does beautifully is engage with the business community, labor leaders and everybody in between.

I was sitting in the Oval Office when a group of executives came in and told us this, Martha. All the stuff that they were going to have on their store shelves during the Christmas holidays had already been bought in dollar contracts.

What does that mean for your viewers? It means that these people did not have any power to basically shift the burden back to China. So, the — the other thing we heard from these business leaders was that, just give us some time to December 15. And, by the way, we are taking all of our sourcing production facilities out of China, and we will continue to do that.